What’s a house for?

In Britain today, and you get two contradictory answers depending on who you ask: a place to live, and a store of wealth for a decent pension that should appreciate for decades.

We have never resolved which of those two things housing actually is - and that unresolved contradiction is the single biggest reason Britain can’t build enough of it.

Net property wealth makes up 40% of total household wealth in Great Britain - the single largest component of wealth.

For most UK households, property and pensions together make up over 80% of everything they own.

It means a large majority of the electorate has a direct, personal financial interest in house prices continuing to rise - which means a direct financial interest in there not being too many new homes built nearby.

Zoom out from household wealth to the whole economy, and the picture gets starker.

McKinsey Global Institute, studying ten major economies including the UK, found that real estate now makes up roughly two-thirds of all global net worth, while infrastructure, machinery, R&D, and technology combined make up only about a fifth.

McKinsey’s own researchers ask the question this raises: are we storing wealth productively?

Their answer points toward capital going into productive investment instead of passive property appreciation as one of the only ways to unwind this without a crisis.

Capital that could be funding new businesses, R&D, equipment, or productive infrastructure is instead parked in existing homes, chasing appreciation on land that already has a house built on it.

We’re taught not to put money under the mattress, to invest it, to use it productively, but that’s exactly what we are doing, except worse, because it also makes the same asset harder for the next generation to buy and raises costs on the whole economy.

The Town & Country Act 1947

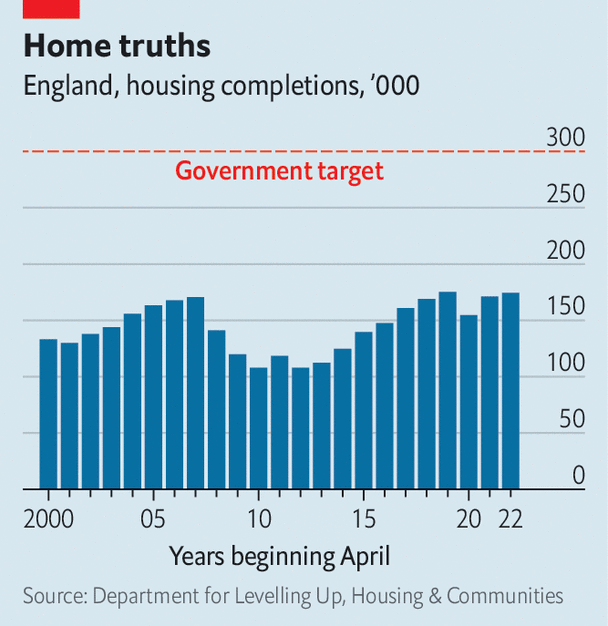

The Town and Country Planning Act 1947 nationalised the right to develop land, replacing a system closer to zoning - build automatically if you meet the rules - with a discretionary one, where every project needs individual, case-by-case permission that can be reopened and contested on subjective grounds almost indefinitely.

Every reform since has tinkered with the paperwork around that decision. None has touched the decision itself.

That mechanism interacts directly with the wealth concentration above, and the two together explain why “build more homes” polls well in the abstract and keeps losing at the specific planning meeting. A discretionary system lets existing residents - who have a direct financial stake in scarcity - object to a specific, named project, while the people who’d benefit from it (the graduate who’d have bought that home, the family priced out of the area) don’t exist yet in any form the system can hear from.

It’s not that nobody wants more housing. It’s that the person defending the specific project standing in a specific field is always outnumbered by the people already living around it, and that asymmetry repeats at every single planning decision, for as long as more people in a constituency already own a home than are trying to buy their first one.

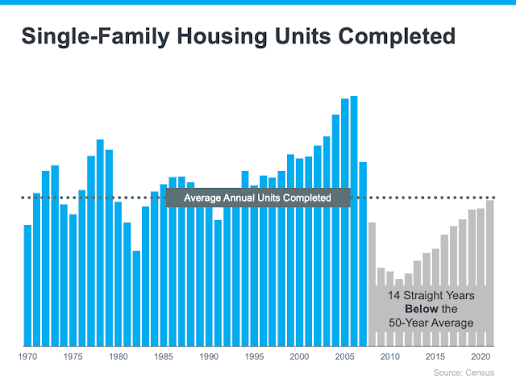

Why the damage compounds

Because housing sits inside almost every other part of the economy, this isn’t a housing-specific problem - it inflates everywhere at once.

A housing shortage raises rents, which raises the cost of hiring in productive cities, which pushes businesses toward cheaper, less productive locations (offshore) which lowers national output.

It shows up in graduate underemployment, in the affordability of starting a family, in the cost of care, in wage demands that outpace productivity because take-home pay increasingly has to cover housing costs first.

It shows up most starkly in the choice young people are making not to have children.

Fertility isn’t something you fix by throwing money at it - it’s a signal, an indicator of whether people believe they have enough resources, enough space, and enough optimism about the future to bring another person into it.

When young people spend their most fertile years commuting long distances, renting, or saving for a deposit that keeps receding, the right time to start a family never quite arrives - or arrives too late to have more than one or two children instead of the number they might have wanted.

That effect, once it’s played out across a generation, is largely irreversible.

Britain’s response to the labour shortage has so far been immigration. A short term fix rather than solving the actual root cause.

They let the illusion of economic growth continue without anyone having to take the short-term pain of admitting that a large share of Britain’s household wealth is built on artificially restricted supply.

Britain’s core economic incentive is GDP growth, and GDP growth is mostly a measure of spending - not of whether that spending reflects anything sustainable or anyone actually being better off.

Rising house prices let people borrow against their homes and spend more.

Higher household debt and lower savings show up as higher GDP growth, regardless of whether the underlying position of the country has actually improved.

Goodhart’s Law: when a measure becomes a target, it ceases to be a good measure.

GDP became the target; housing-driven debt became one of the easiest ways to hit it; and the fact that this comes at the cost of future capacity - fewer children, a hollowed-out productive base, young adults locked out of ownership - simply doesn’t show up in the number we’re all optimising for.

Also Britain treats public debt as something to be feared and constrained, while private mortgage debt of the same scale, built on the same restricted supply of housing, is treated as perfectly normal- even as the foundation of a “healthy” property-owning economy.

Housing As Infrastructure

Housing should be treated as infrastructure, not a place to grow money.

The definition of infrastructure is the foundational structure a society needs to function - and by that definition, housing belongs in the same category as roads and energy, not in the same category as shares and pensions.

Like a road, a home should be judged by whether it lets someone get somewhere - into a stable life, a career, a family - not by whether it’s worth more this year than last, and how it helps society to flourish.

Nobody argues we should grow the economy by raising tolls on roads.

If Britain built abundant housing and let capital that’s currently parked in property flow into genuinely productive investment instead, it would produce a real and sustainable economic expansion.

That window is still open, but it’s closing.

While we wait, we all pay the cost.

And a talented, educated generation, quietly fades away into old age, families have fewer kids and talent moves overseas.

Every year it stays unaddressed, it gets narrower, and some of its costs - the households that were never formed, the children who were never had - don’t come back once the window closes.

Tell me where this is wrong.