Growing to Oblivion - From Suicidal Economics To Unimaginable Abundance

Resolving the Economic Contradiction and The Great Awakening

We live in an era where our economic success is increasingly disconnected from reality.

Gross Domestic Product (GDP) skyrockets, stock markets boom.

Yet, birth rates plummet, families struggle with unaffordable housing, the deficit keeps rising uncontrollably each year.

This is our economic contradiction.

Why is everything getting better, technology booming, but these indicators demonstrate otherwise? Shouldn’t our deficit be falling and birth rates growing?

At the heart of it is a bug in our economics - it’s suicidal economics - a system that grows by liquidating long-term human flourishing.

The importance of incentives

I’ll start and finish with the importance of incentives as Charlie Munger mentioned, and then introduce the solution by coming back to Warren Buffet.

Show me the incentive and I'll show you the outcome. Charlie Munger

In this article I’m going to explain the history of various forms of economic incentives over time and GDP and how it came about.

The Spanish Empire Plundering Gold

In 1790 Spain was the largest power in the world, it benefited from accumulating huge amounts of gold and silver.

But the problem is, when the resources stopped, there was nothing to fall back on, it failed to develop local industry - it didn’t need to. It was overtaken by the next power with a better philosophy.

The British Empire Industrialised

The British saw it differently - national wealth comes from a nation's productive capacity - not by the amount of resources it could accumulate but by how much it could create. The wealth of nations was written in 1776. Britain became the workshop of the world

The First Industrialist's Dilemma - Britain failed to pivot away from declining heavy, export-oriented industries (coal, shipbuilding, iron, textiles) and US, Germany had natural advantages in industry and resources and overtook and didn’t need to maintain global expensive sea routes. The railroad was more efficient than the sea empire. Britain was burdened by a large empire and failed to move toward emerging consumer-oriented sectors, resulting in mass industrial over-capacity, obsolete techniques, and high unemployment

The US Consumer Economy

In 1934, in the aftermath of the great depression, the US adopted a new philosophy - GDP. An economy was measured by the volume of activity and transactions in the economy. Consumerism was born, and then, the welfare state.

Every 100 or so years we have a fundamental shift in how things work and now we are coming to an end to the consumer period and need a new economic model. The industrial era economics that are focused on the consumer economy no longer work.

We now have the internet and that means a completely different system. In 2026, this philosophy is now gutting out local industry, and fail to differentiate between good and bad transactions.

The Problem with GDP

“GDP measures everything, in short, except that which makes life worthwhile.” - Robert F. Kennedy

GDP was designed to measure how fast the economy is moving and how many transactions are happening. It is exactly like the speedometer on a car. It doesn’t measure how strong the economy is and how much it is actually growing, just how fast it is currently moving.

This is a great measure when the economy is operating at 10 - 70mph, but when it reaches the outer limits, it becomes damaging to the engine. It incentivises taking on more debt, to go faster and to keep going at any speed. It’s a good measure in principle, but when it’s the overriding pricniple, it becomes damaging.

Any damn fool can overtake going downhill!

Why upgrading our economic engine sometimes means slowing down the car.

In order to upgrade the economy, we need to look at and actually upgrade the car engine.

The Rear-View Mirror Trap

Beyond the speed analogy, the fatal flaw of GDP is that it is fundamentally backward-looking. It measures the “smoke” of yesterday’s fire but tells you nothing about the fuel left for tomorrow.

Because GDP only registers a “success” when money changes hands now, it creates a perverse incentive to liquidate the future to pay for the present. We sell off our natural resources, we over-leverage our children with debt, and we burn through the “social capital” of the family unit - all to keep the current quarter’s numbers high. It is the economic equivalent of a farmer eating his seed corn to feel full today, then wondering why he is starving when the next season arrives.

This isn't just a radical critique; it’s a realization reaching the highest levels of global thought. Joseph Stiglitz, a Nobel laureate, has long argued that GDP is a poor measure of well-being because it ignores inequality and sustainability. Similarly, the World Economic Forum and the OECD have begun developing "Beyond GDP" frameworks, acknowledging that measuring "transactions" while ignoring the depletion of natural and human capital is like a pilot flying a plane by looking only at the fuel flow and ignoring the altimeter.

GDP Eats the Family

Economies focused on maximizing GDP naturally also seek to move activity from the informal sector (home, community, unpaid care) into the formal sector (taxable transactions).

In a traditional family structure, “care” is a non-monetized consumer surplus. When a mother cares for a child, or a family cooks a meal together, no GDP is recorded. However, when the State provides childcare or a corporation delivers a meal via an app, GDP rises.

This creates a systemic incentive for the State to “eat into” the family’s role, replacing organic bonds with institutional or transactional ones.

Social psychologist Jon Haidt refers to this shift as the ‘Great Rewiring.’ By moving childhood and community from the real-world ‘informal sector’ onto algorithmically optimized digital platforms, we have traded the mental health of an entire generation for a temporary boost in engagement metrics.

GDP acts as a master incentive on the economy. Directly - as state spending is 40% of the economy, but also through the control of policy in the parts - immigration, limiting housing, and education.

As the economy seeks new frontiers for growth, it has begun to “financialize” human relationships. The “consumer surplus” of dating and companionship is being harvested by platforms designed to maximize engagement and profit.

Tinder and the Dating Market: What was once a community-based social process is now an algorithmically driven market. This has led to a “winner-take-all” dynamic that leaves many men feeling economically and socially devalued.

OnlyFans and the Commodity of Attention: The monetization of intimacy (OnlyFans) and the gamification of attention (smartphones/social media) turn human connection into a series of micro-transactions.

The end goal of an economy seeking total GDP growth is a society of perfectly atomized individuals who depend entirely on the Market and the State for every need, from food to emotional validation.

The Abundance of the Digital Economy

As economist Diane Coyle, author of GDP: A Brief but Affectionate History, argues: “GDP was designed for a world of mass-produced physical goods. It is fundamentally ill-equipped to measure a digital economy where the most valuable assets—data, software, and human connection - often have a market price of zero but a societal value that is infinite.”

The conflict we have now is that the consumer economy measures transactions in terms of price, but the value is decreasingly connected to the price. Digital economics result in everything becoming cheaper over time.

This creates the very peverse incentive of governments who are seeking GDP growth to:

Increase debt

Create artificial scarcity to maintain the price of certain goods, and keep the economy growing.

So now I’m going to explore two examples that are dangerous and the reasons behind them.

Governments Restrict Housing to Keep the Economy Strong

There is a conflict between young people getting on the housing ladder and the economy.

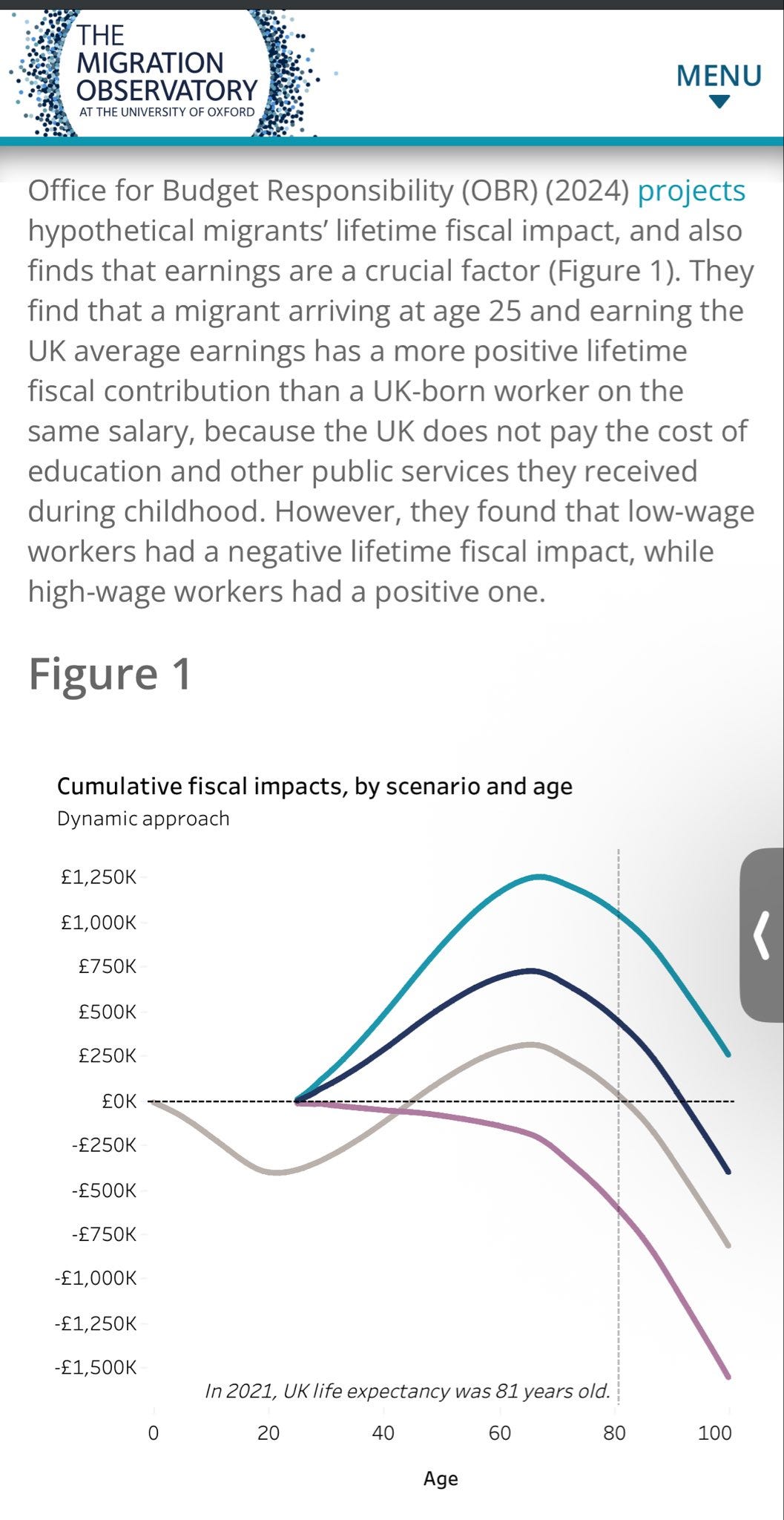

Immigration is Better for the Economy

The Migration Observatory and Office of Budget Responsibility have written about how immigration is better for the economy because the country doesn’t need to cover the costs of raising the person from a baby. It boosts the GDP

https://migrationobservatory.ox.ac.uk/resources/briefings/the-impact-of-migration-on-uk-population-growth/

This demonstrates the perverse incentive that exists to limit the number of new people who are being born and import people from other countries, effectively removing the cost.

Demographic researcher Stephen J Shaw , director of Birthgap, has identified that this ‘unplanned childlessness’ is a byproduct of economic shocks that force young people to delay family-building until the biological window begins to close - a cost that GDP never accounts for.

Large scale immigration also creates a self-reinforcing cycle where the competition on housing also increases costs to raise a family and limits the amount of new children that can grow. This forces a downward pressure on populations.

Companies Also Have an Incentives to Limit Population

Larry Fink CEO of Blackrock, one of the most influential figures in global finance, that owns leading stakes in many of the world’s biggest companies highlights how lower birth rates is an advantage for an economy as it requires them to develop automation and industry.

This shows how is there is an aligned incentive of companies, shareholders, and nations to restrict the population and bring in robots an AI. The more that gap, the more that is needed.

It’s essential to be mindful of that interest and how that is also driven by companies incentives to fill the gap.

The Importance of Humans

A declining birth rates is not an inevitable thing but the result of specific policies and the result of the master incentives. At no point in our GDP do we consider humans as valuable, and so we are liquidating humans.

The Economy of Completely AI

Taken to the extreme - if we have an economy that is made fully of robots and AI, it can become completely about resource extraction, energy and then selling to humans or other AI.

If robots do all the work, humans have no wages. If humans have no wages, they cannot buy what the robots produce. If no one buys what is produced, the "economy" (as measured by transactions) collapses

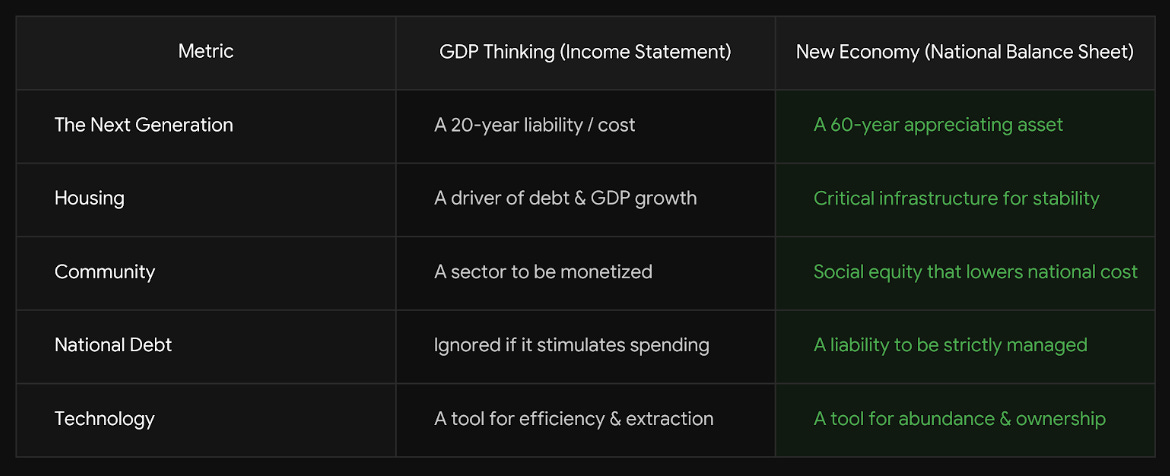

The Solution - the Balance Sheet

We need a reboot of what a human is for in the economy. And this also comes to the heart of what economics is about - from allocating finite resources in the face of infinite consumer needs towards creating abundance. Humans are not a consumer, but the heart of the new economy. Human capital is the core pillar of the economy.

On an Income Statement (GDP), a child is a 20-year liability. On a Balance Sheet, a child is a 60-year appreciating asset. When we change the math, we change the incentive to support families, education and healthcare.

As our economy is maturing, it’s essential to move away from thinking of the economy as a speedometer and moving towards measuring the economy as a balance sheet.

Warren Buffet: “I spend more time looking at balance sheets than I do income statements”.

Lowering house prices and building more houses would make the GDP fall but would grow birth rates and grow the balance sheet.

So, what does a National Balance Sheet actually look like? Unlike GDP, which only tracks ‘Activity,’ a Balance Sheet tracks Net Worth.

Assets: We would list our ‘Human Capital’ (birth rates and cognitive health), our ‘Resource Equity’ (energy independence), and our ‘ Infrastructure’ (housing affordability and family stability).

Liabilities: We track not just fiscal debt (and actually measure and incentivise managing it - because GDP completely omits it), but ‘Social Depreciation’—the rising costs of loneliness, mental health crises, and the hollowing out of our local communities.

Conclusion

If we follow Charlie Munger’s logic, our current 'Suicidal Economics' are simply the result of a bad incentive: the obsession with the GDP speedometer. To fix the outcome, we must change the incentive. By shifting our gaze from the 'Income Statement' of today to the 'Balance Sheet' of tomorrow, as Warren Buffett does, we stop liquidating our future to pay for our present. We stop being a consumer-driven engine and start being a human-driven legacy.

In the end, a civilization that optimizes for a speedometer while the gas tank is empty isn't 'growing'- it's just coasting toward a cliff in high gear

How should we navigate the current reality and prepare for and build this future

Further Reading

This thesis builds upon the work of several thinkers who are already sounding the alarm on our current economic “operating system.” For those looking to dive deeper into the “Beyond GDP” movement and the future of human capital, I highly recommend:

Noah Smith on why productivity and birth rates are the true engines of a nation.

kyla scanlon on the “disconnect” between economic data and human reality

Ted Gioia on the “Financialization of Culture” (which aligns with “GDP Eats the Family” section).

Jon Haidt – On how technology is "liquidating" the mental health of the youth

Jordan B Peterson – On the importance of family units as the core of society.

Rory Sutherland – On why “psychological value” matters more than “market price.”

(Pronatalist.org) – Leading voices on the birth rate crisis

Stephen J Shaw Stephen J. Shaw (Director of Birthgap) – Documentary filmmaker on demographic collapse

Diane Coyle - Why the economy feels broken even when its growing Podcast, and Blog.